From day one, the problem we wanted to solve was how to predict and generate sales growth. Or more succinctly, how to figure how to win more customers.

Our initial 12 clients ─ Aramark, Chili’s Restaurants, Cingular Wireless, Coors, Cymer, Equifax, General Motors, i2 Technologies, IBM, Sabre Systems, Sikorsky Aircraft, and Tony Robbins ─ provided us with a cross-section of industries to kick off our analysis of how to connect customer perceptions with a company’s sales growth.

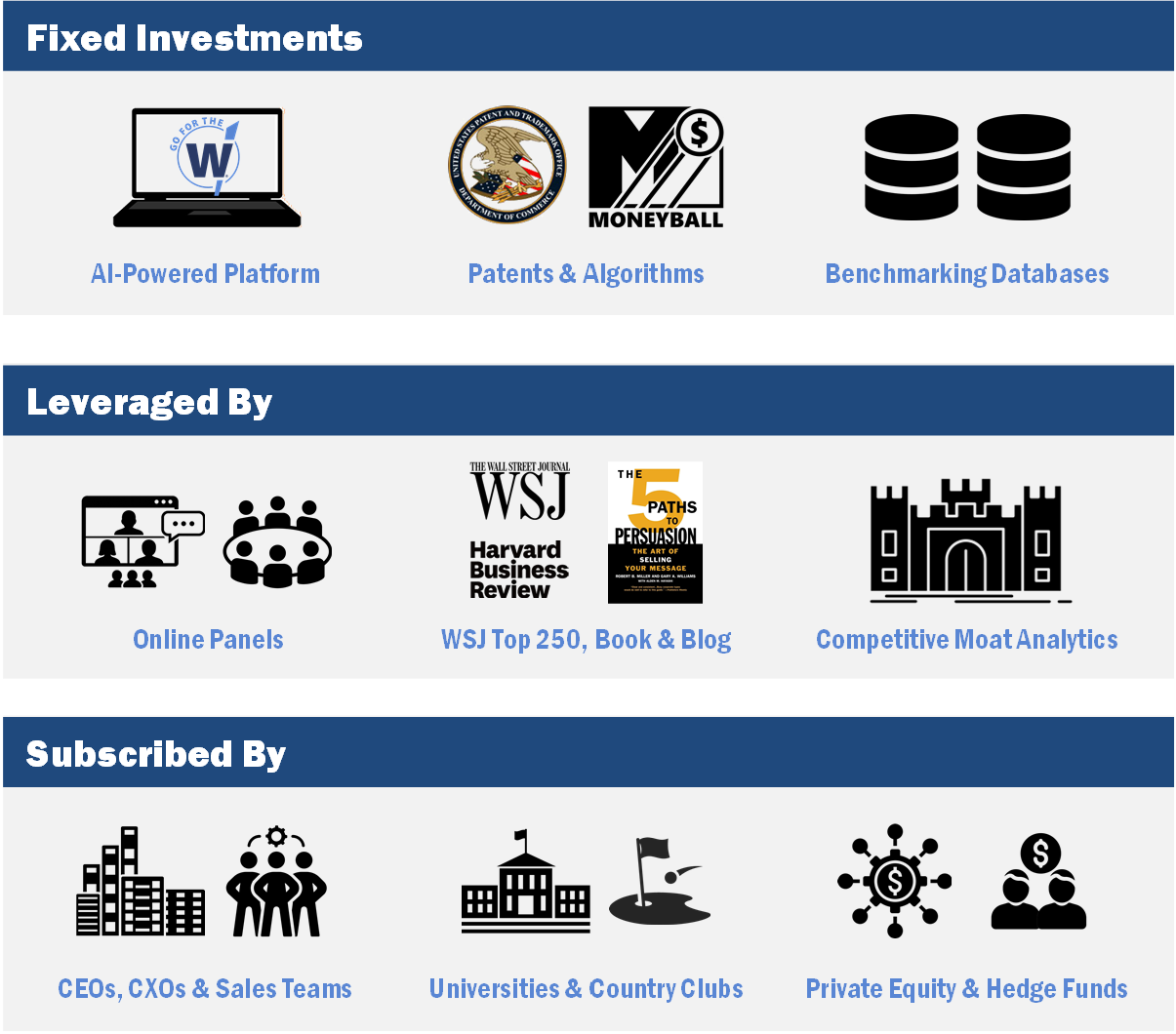

Today, we make a series of fixed investments every year, leveraged by key aspects in our business, and subscribed to by CEOs/CXOs/Sales Teams, Universities & Country Clubs, and PE Firms & Hedge Funds.

To our knowledge, we are the only firm that measures the competitive strength of companies based on customer expectations, company performance and pricing power.